Use these links to rapidly review the document

TABLE OF CONTENTS

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

Form 10-Q

| (Mark One) | |

ý |

QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended June 30, 2005 |

|

OR |

|

o |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to |

|

Commission file number 001-32427

HUNTSMAN CORPORATION

(Exact name of registrant as specified in its charter)

| Delaware (State or other jurisdiction of incorporation or organization) |

42-1648585 (I.R.S. Employer Identification No.) |

|

500 Huntsman Way Salt Lake City, Utah 84108 (801) 584-5700 (Address of principal executive offices and telephone number) |

||

Indicate by check mark whether the Registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. YES ý NO o

Indicate by check mark whether the Registrant is an accelerated filer (as defined in Exchange Act Rule 12b-2). YES o NO ý

On August 10, 2005, 220,451,484 shares of common stock of the Registrant were outstanding.

HUNTSMAN CORPORATION AND SUBSIDIARIES

QUARTERLY REPORT ON FORM 10-Q FOR THE QUARTERLY PERIOD

ENDED JUNE 30, 2005

HUNTSMAN CORPORATION AND SUBSIDIARIES

CONDENSED CONSOLIDATED BALANCE SHEETS (UNAUDITED)

(In Millions, Except Share Amounts)

| |

June 30, 2005 |

December 31, 2004 |

|||||||

|---|---|---|---|---|---|---|---|---|---|

| ASSETS | |||||||||

| Current assets: | |||||||||

| Cash and cash equivalents | $ | 251.5 | $ | 243.5 | |||||

| Restricted cash | 13.5 | 8.9 | |||||||

| Accounts and notes receivable (net of allowance for doubtful accounts of $25.2 and $25.8, respectively) | 1,515.7 | 1,545.4 | |||||||

| Accounts receivable from affiliates | 4.3 | 12.1 | |||||||

| Inventories, net | 1,311.2 | 1,253.9 | |||||||

| Prepaid expenses | 21.1 | 45.0 | |||||||

| Deferred income taxes | 11.8 | 11.9 | |||||||

| Other current assets | 79.2 | 65.5 | |||||||

| Total current assets | 3,208.3 | 3,186.2 | |||||||

Property, plant and equipment, net |

4,808.4 |

5,150.9 |

|||||||

| Investment in unconsolidated affiliates | 178.8 | 170.9 | |||||||

| Intangible assets, net | 227.6 | 245.6 | |||||||

| Goodwill | 3.3 | 3.3 | |||||||

| Deferred income taxes | 41.3 | 34.5 | |||||||

| Notes receivable from affiliates | 9.5 | 23.6 | |||||||

| Other noncurrent assets | 604.5 | 608.5 | |||||||

| Total assets | $ | 9,081.7 | $ | 9,423.5 | |||||

| LIABILITIES AND STOCKHOLDERS' EQUITY (DEFICIT) | |||||||||

| Current liabilities: | |||||||||

| Accounts payable | $ | 994.0 | $ | 994.9 | |||||

| Accounts payable to affiliates | 8.7 | 30.6 | |||||||

| Accrued liabilities | 632.1 | 754.4 | |||||||

| Deferred income taxes | 14.4 | 10.8 | |||||||

| Current portion of long-term debt | 78.0 | 37.5 | |||||||

| Total current liabilities | 1,727.2 | 1,828.2 | |||||||

Long-term debt |

4,628.6 |

6,221.1 |

|||||||

| Long-term debt to affiliates | — | 40.9 | |||||||

| Deferred income taxes | 210.3 | 217.9 | |||||||

| Other noncurrent liabilities | 807.8 | 757.1 | |||||||

| Total liabilities | 7,373.9 | 9,065.2 | |||||||

| Minority interests in common stock of consolidated subsidiaries | 43.9 | 36.8 | |||||||

| Warrants issued by consolidated subsidiary | — | 128.7 | |||||||

| Redeemable preferred members' interest | — | 574.8 | |||||||

Commitments and contingencies (Notes 17 and 18) |

|||||||||

Stockholders' equity (deficit): |

|||||||||

| Common stock $0.01 par value, 1,200,000,000 shares authorized, 221,200,997 issued and 220,451,484 outstanding | 2.2 | — | |||||||

| Preferred members' interest | — | 195.7 | |||||||

| Mandatory convertible preferred stock $0.01 par value, 100,000,000 shares authorized, 5,750,000 issued and outstanding | 287.5 | — | |||||||

| Additional paid-in capital | 2,774.7 | 712.5 | |||||||

| Unearned stock-based compensation | (15.0 | ) | — | ||||||

| Accumulated deficit | (1,414.9 | ) | (1,471.2 | ) | |||||

| Accumulated other comprehensive income | 29.4 | 181.0 | |||||||

| Total stockholders' equity (deficit) | 1,663.9 | (382.0 | ) | ||||||

| Total liabilities and stockholders' equity (deficit) | $ | 9,081.7 | $ | 9,423.5 | |||||

See accompanying notes to unaudited condensed consolidated financial statements.

1

HUNTSMAN CORPORATION AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS AND

COMPREHENSIVE INCOME (LOSS) (UNAUDITED)

(In Millions, Except Per Share Amounts)

| |

Three months ended June 30, |

Six Months Ended June 30, |

|||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2005 |

2004 |

2005 |

2004 |

|||||||||||

| Revenues: | |||||||||||||||

| Trade sales | $ | 3,264.6 | $ | 2,740.2 | $ | 6,577.1 | $ | 5,354.5 | |||||||

| Related party sales | 74.9 | 13.8 | 111.7 | 20.3 | |||||||||||

| Total revenues | 3,339.5 | 2,754.0 | 6,688.8 | 5,374.8 | |||||||||||

| Cost of goods sold | 2,830.0 | 2,420.0 | 5,590.2 | 4,761.1 | |||||||||||

| Gross profit | 509.5 | 334.0 | 1,098.6 | 613.7 | |||||||||||

Operating Expenses: |

|||||||||||||||

| Selling, general and administrative | 174.7 | 163.8 | 332.3 | 330.2 | |||||||||||

| Research and development | 25.6 | 22.8 | 49.9 | 49.2 | |||||||||||

| Other operating expense | 5.3 | 27.6 | 50.0 | 20.1 | |||||||||||

| Restructuring and plant closing costs | 18.8 | 150.5 | 29.2 | 159.2 | |||||||||||

| Total operating expenses | 224.4 | 364.7 | 461.4 | 558.7 | |||||||||||

| Operating income (loss) | 285.1 | (30.7 | ) | 637.2 | 55.0 | ||||||||||

Interest expense, net |

(101.1 |

) |

(144.9 |

) |

(240.7 |

) |

(304.9 |

) |

|||||||

| Loss on accounts receivable securitization program | (2.4 | ) | (3.0 | ) | (5.6 | ) | (6.5 | ) | |||||||

| Equity in income of unconsolidated affiliates | 2.9 | 2.4 | 5.2 | 3.1 | |||||||||||

| Other expense | (2.5 | ) | (2.1 | ) | (235.8 | ) | (3.9 | ) | |||||||

| Income (loss) before income taxes and minority interest | 182.0 | (178.3 | ) | 160.3 | (257.2 | ) | |||||||||

| Income tax expense | (29.0 | ) | (5.5 | ) | (61.1 | ) | (10.4 | ) | |||||||

| Income (loss) before minority interest income (loss) | 153.0 | (183.8 | ) | 99.2 | (267.6 | ) | |||||||||

| Minority interest in subsidiaries' income (loss) | 0.1 | (0.7 | ) | 0.1 | (0.9 | ) | |||||||||

| Income (loss) from continuing operations | 153.1 | (184.5 | ) | 99.3 | (268.5 | ) | |||||||||

Loss from discontinued operations (including loss on pending disposal of $36.4 in 2005), net of tax |

(40.4 |

) |

(0.9 |

) |

(43.0 |

) |

(1.7 |

) |

|||||||

| Net income (loss) | 112.7 | (185.4 | ) | 56.3 | (270.2 | ) | |||||||||

| Preferred stock dividends | — | (21.9 | ) | (43.1 | ) | (43.8 | ) | ||||||||

| Net income (loss) available to common stockholders | $ | 112.7 | $ | (207.3 | ) | $ | 13.2 | $ | (314.0 | ) | |||||

| Net income (loss) | $ | 112.7 | $ | (185.4 | ) | $ | 56.3 | $ | (270.2 | ) | |||||

| Other comprehensive loss | (105.0 | ) | (14.0 | ) | (151.6 | ) | (20.9 | ) | |||||||

| Comprehensive income (loss) | $ | 7.7 | $ | (199.4 | ) | $ | (95.3 | ) | $ | (291.1 | ) | ||||

| Basic income (loss) per share: | |||||||||||||||

| Income (loss) from continuing operations | $ | 0.69 | $ | (0.94 | ) | $ | 0.25 | $ | (1.41 | ) | |||||

| Loss from discontinued operations, net of tax | (0.18 | ) | — | (0.19 | ) | (0.01 | ) | ||||||||

| Net income (loss) | $ | 0.51 | $ | (0.94 | ) | $ | 0.06 | $ | (1.42 | ) | |||||

| Weighted average shares | 220.5 | 220.5 | 220.5 | 220.5 | |||||||||||

| Diluted income (loss) per share: | |||||||||||||||

| Income (loss) from continuing operations | $ | 0.66 | $ | (0.94 | ) | $ | 0.25 | $ | (1.41 | ) | |||||

| Loss from discontinued operations, net of tax | (0.18 | ) | — | (0.19 | ) | (0.01 | ) | ||||||||

| Net income (loss) | $ | 0.48 | $ | (0.94 | ) | $ | 0.06 | $ | (1.42 | ) | |||||

| Weighted average shares | 233.0 | 220.5 | 220.5 | 220.5 | |||||||||||

See accompanying notes to unaudited condensed consolidated financial statements.

2

HUNTSMAN CORPORATION AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENT OF STOCKHOLDERS' EQUITY (DEFICIT)

(UNAUDITED)

(In Millions, Except Share Amounts)

| |

Shares |

|

|

|

|

|

|

|

|

||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

Common stock |

Mandatory convertible preferred stock |

Common stock |

Preferred members' interest |

Mandatory convertible preferred stock |

Additional paid-in capital |

Unearned stock- based compensation |

Accumulated deficit |

Accumulated other comprehensive income (loss) |

Total |

|||||||||||||||||||

| Balance, January 1, 2005 | — | — | $ | — | $ | 195.7 | $ | — | $ | 712.5 | $ | — | $ | (1,471.2 | ) | $ | 181.0 | $ | (382.0 | ) | |||||||||

| Net income | — | — | — | — | — | — | — | 56.3 | — | 56.3 | |||||||||||||||||||

| Other comprehensive loss | — | — | — | — | — | — | — | — | (151.6 | ) | (151.6 | ) | |||||||||||||||||

| Issuance of common stock and mandatory convertible preferred stock | 69,261,365 | 5,750,000 | 2.2 | — | 287.5 | 1,199.4 | — | — | 1,489.1 | ||||||||||||||||||||

| Issuance of restricted stock awards | — | — | — | — | — | 16.9 | (16.9 | ) | — | — | — | ||||||||||||||||||

| Recognition of stock-based compensation | — | — | — | — | — | 1.9 | 1.9 | — | — | 3.8 | |||||||||||||||||||

| Exchange of previous common and preferred members' interest and warrants for common stock | 151,190,119 | — | — | (195.7 | ) | — | 887.1 | — | — | — | 691.4 | ||||||||||||||||||

| Dividends declared on mandatory convertible preferred stock | — | — | — | — | — | (43.1 | ) | — | — | — | (43.1 | ) | |||||||||||||||||

| Balance, June 30, 2005 | 220,451,484 | 5,750,000 | $ | 2.2 | $ | — | $ | 287.5 | $ | 2,774.7 | $ | (15.0 | ) | $ | (1,414.9 | ) | $ | 29.4 | $ | 1,663.9 | |||||||||

See accompanying notes to unaudited condensed consolidated financial statements.

3

HUNTSMAN CORPORATION AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS (UNAUDITED)

(Dollars in Millions)

| |

Six months ended June 30, |

|||||||

|---|---|---|---|---|---|---|---|---|

| |

2005 |

2004 |

||||||

| Operating Activities: | ||||||||

| Net income (loss) | $ | 56.3 | $ | (270.2 | ) | |||

| Adjustments to reconcile net income (loss) to net cash provided by operating activities: | ||||||||

| Equity in income of investment in unconsolidated affiliates | (5.2 | ) | (3.1 | ) | ||||

| Depreciation and amortization | 249.4 | 279.3 | ||||||

| Noncash restructuring and plant closing costs | 0.1 | 81.1 | ||||||

| (Reversal of) provision for losses on accounts receivable | (3.9 | ) | 2.6 | |||||

| Loss (gain) on disposal of assets | 1.1 | (0.2 | ) | |||||

| Loss on pending disposal of discontinued operations | 36.4 | — | ||||||

| Loss on early extinguishment of debt | 235.0 | 4.2 | ||||||

| Non-cash interest expense | 37.6 | 60.2 | ||||||

| Deferred income taxes | 28.1 | 18.3 | ||||||

| Net unrealized losses (gains) on foreign currency transactions | 12.6 | (13.5 | ) | |||||

| Other | (10.4 | ) | 1.3 | |||||

| Changes in operating assets and liabilities: | ||||||||

| Accounts and notes receivables | 71.6 | (203.7 | ) | |||||

| Change in receivables sold, net | 4.1 | 29.7 | ||||||

| Inventories | (79.9 | ) | (1.9 | ) | ||||

| Prepaid expenses | 27.5 | 20.2 | ||||||

| Other current assets | (7.6 | ) | (26.9 | ) | ||||

| Other noncurrent assets | 9.2 | (67.7 | ) | |||||

| Accounts payable | (61.9 | ) | 73.8 | |||||

| Accrued liabilities | (113.2 | ) | 49.4 | |||||

| Other noncurrent liabilities | (32.0 | ) | 13.1 | |||||

| Net cash provided by operating activities | 454.9 | 46.0 | ||||||

| Investing Activities: | ||||||||

| Capital expenditures | (128.7 | ) | (94.2 | ) | ||||

| Proceeds from sale of assets | 4.8 | 1.7 | ||||||

| Investments in unconsolidated affiliates | (9.1 | ) | (11.8 | ) | ||||

| Acquisition of minority interests | — | (7.2 | ) | |||||

| Net cash received from unconsolidated affiliates | 0.7 | 8.3 | ||||||

| Investment in government securities | (40.9 | ) | — | |||||

| Advances to unconsolidated affiliates | — | (1.2 | ) | |||||

| Change in restricted cash | (4.6 | ) | — | |||||

| Net cash used in investing activities | (177.8 | ) | (104.4 | ) | ||||

| Financing Activities: | ||||||||

| Net (repayment) borrowings under revolving loan facilities | (53.0 | ) | 89.3 | |||||

| Net repayments of overdraft and other short term debt | (14.9 | ) | (7.8 | ) | ||||

| Repayment of long-term debt | (1,584.1 | ) | (431.2 | ) | ||||

| Call premiums related to early extinguishment of debt | (106.7 | ) | — | |||||

| Debt issuance costs | (0.4 | ) | (12.1 | ) | ||||

| Shares issued to minority shareholders for cash | 3.6 | 2.7 | ||||||

| Dividends paid on mandatory convertible preferred stock | (3.6 | ) | — | |||||

| Other | 6.8 | — | ||||||

| Net proceeds from issuance of common and preferred stock | 1,489.1 | 400.0 | ||||||

| Net cash (used in) provided by financing activities | (263.2 | ) | 40.9 | |||||

| Effect of exchange rate changes on cash | (5.9 | ) | (3.7 | ) | ||||

| Increase (decrease) in cash and cash equivalents | 8.0 | (21.2 | ) | |||||

| Cash and cash equivalents at beginning of period | 243.5 | 208.3 | ||||||

| Cash and cash equivalents at end of period | $ | 251.5 | $ | 187.1 | ||||

| Supplemental cash flow information: | ||||||||

| Cash paid for interest | $ | 211.4 | $ | 223.4 | ||||

| Cash paid for income taxes | $ | 13.7 | $ | 1.2 | ||||

See accompanying notes to unaudited condensed consolidated financial statements.

4

HUNTSMAN CORPORATION AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (UNAUDITED)

1. General

Certain Definitions

"Company," "our," "us" or "we" may be used to refer to Huntsman Corporation and, unless the context otherwise requires, its subsidiaries and predecessors. Any references to the "Company," "we," "us" or "our" as of a date prior to October 19, 2004 (the date of our formation) are to Huntsman Holdings, LLC and its subsidiaries (including their respective predecessors). In this report, "HMP" refers to HMP Equity Holdings Corporation (our 100% owned subsidiary that has been merged into our Company), "HLLC" or "Huntsman LLC" refers to Huntsman LLC (our 100% owned subsidiary) and, unless the context otherwise requires, its subsidiaries, "Huntsman Specialty" refers to Huntsman Specialty Chemicals Corporation (a 100% owned subsidiary of HLLC), "HCCA" refers to Huntsman Chemical Company Australia Pty. Ltd. (a 100% owned indirect subsidiary of HLLC) and, unless the context otherwise requires, its subsidiaries, "HIH" refers to Huntsman International Holdings LLC (a subsidiary, which as of June 30, 2005, is owned 58% by us and 42% by HLLC) and, unless the context otherwise requires, its subsidiaries, "HI" refers to Huntsman International LLC (a 100% owned subsidiary of HIH) and, unless the context otherwise requires, its subsidiaries, "AdMat" refers to Huntsman Advanced Materials LLC (our 90.3% owned indirect subsidiary) and, unless the context otherwise requires, its subsidiaries, "Vantico" refers to Vantico Group S.A. (a 100% owned subsidiary of AdMat) and, unless the context otherwise requires, its subsidiaries, "Investments Trust" refers to HMP Equity Trust (a 59% holder of our common stock), "Huntsman Family Holdings" refers to Huntsman Family Holdings LLC (an owner with MatlinPatterson of Investments Trust), "MatlinPatterson" refers to MatlinPatterson Global Opportunities Partners L.P., MatlinPatterson Global Opportunities Partners (Bermuda) L.P. and MatlinPatterson Global Opportunities Partners B L.P. (collectively, an owner with Huntsman Family Holdings of Investments Trust), and "ICI" refers to Imperial Chemical Industries PLC (a former indirect owner of certain of HIH's membership interests) and its subsidiaries.

Description of Business

We are among the world's largest global manufacturers of differentiated and commodity chemical products. We manufacture a broad range of chemical products and formulations, which we market in more than 100 countries to a diversified group of consumer and industrial customers. Our products are used in a wide range of applications, including those in the adhesives, aerospace, automotive, construction products, durable and non-durable consumer products, electronics, medical, packaging, paints and coatings, power generation, refining and synthetic fiber industries. We are a leading global producer in many of our key product lines, including MDI, amines, surfactants, epoxy-based polymer formulations, maleic anhydride and titanium dioxide.

Company

We were formed in 2004 to hold, among other things, the equity interests of Huntsman LLC, HIH and AdMat. The transfer to us of the net assets of Huntsman LLC, HIH and AdMat was between entities under common control and recorded at historical carrying value. Our condensed consolidated financial statements presented herein reflect the financial position, results of operations and cash flows as if Huntsman LLC, HIH, AdMat and our Company were combined for all periods presented.

On February 16, 2005, we completed an initial public offering of 55,681,819 shares of our common stock sold by us and 13,579,546 shares of our common stock sold by a selling stockholder, in each case at a price to the public of $23 per share, and 5,750,000 shares of our 5% mandatory convertible preferred stock sold by us at a price to the public of $50 per share. Each share of preferred stock will

5

be convertible into between approximately 1.77 and approximately 2.17 shares of our common stock, subject to anti-dilution adjustments, depending upon the trading price of our common stock prior to the third anniversary of our initial public offering. This will result in between approximately 10.2 million and approximately 12.5 million additional shares of our common stock outstanding upon conversion. See "Note 24—Net Income (Loss) per Share."

The net proceeds to us from our initial public offering of common and preferred stock were approximately $1,500 million, substantially all of which has been used to repay outstanding indebtedness of certain of our subsidiaries, including HMP, Huntsman LLC and HIH, as follows:

In connection with the repayment of indebtedness, we recorded a loss on early extinguishment of debt in the three and six months ended June 30, 2005 of $2.0 million and $235.0 million, respectively.

In connection with the completion of our initial public offering, we consummated a reorganization transaction (the "Reorganization Transaction"). In the Reorganization Transaction, our predecessor, Huntsman Holdings, LLC, became our wholly owned subsidiary, and the existing beneficial holders of the common and preferred membership interests of Huntsman Holdings, LLC received shares of our common stock in exchange for their interests.

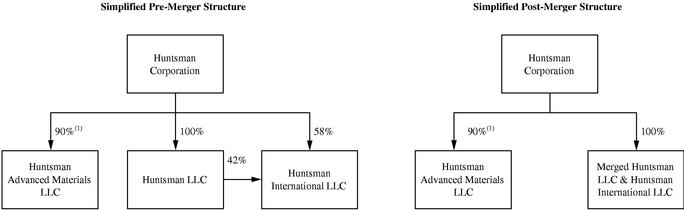

As a result of our cash contributions that were used to redeem the HIH Senior Discount Notes and our contribution to HIH of the senior subordinated reset discount notes due 2009 of HIH that were originally issued to ICI (the "HIH Senior Subordinated Discount Notes"), our ownership interest in HIH increased from 40% to 58%, and, accordingly, Huntsman LLC's interest in HIH decreased from 60% to 42%.

In connection with our initial public offering and as part of the Reorganization Transaction, we exercised our right under the outstanding warrants to purchase common stock of HMP (the "HMP Warrants") to require that all the HMP Warrants and any shares of HMP issued upon exercise of the HMP Warrants be exchanged for newly issued shares of our common stock. Under the terms of the HMP Warrants, an aggregate of approximately 16.8 million shares of our common stock was issued in exchange for the outstanding HMP Warrants on March 14, 2005.

Investments Trust holds approximately 59% of our common stock. Jon M. Huntsman and Peter R. Huntsman control the voting of the shares of our common stock held by Investments Trust. However,

6

the shares of our common stock held by Investments Trust will not be voted in favor of certain fundamental corporate actions without the consent of MatlinPatterson, through its representatives David J. Matlin or Christopher R. Pechock, and Jon M. Huntsman and Peter R. Huntsman have agreed to cause all of the shares of our common stock held by Investments Trust to be voted in favor of the election to our board of directors of two nominees designated by MatlinPatterson.

Proposed Merger of Huntsman LLC into Huntsman International LLC and Proposed New Credit Facility

In July 2005, we obtained the required consents from the holders of Huntsman LLC's senior secured notes and senior notes to amend certain provisions in the indentures governing these notes. The amendments will facilitate the proposed merger of Huntsman LLC with and into HI. The amendments include, among other things, the increase in the amount of secured indebtedness Huntsman LLC can incur. In addition, with respect to Huntsman LLC's senior secured notes, the amendment also provides for the elimination of stock pledges of subsidiaries as collateral under the applicable indentures.

The proposed merger of Huntsman LLC with and into HI will help simplify our financing and reporting structure and is expected to facilitate other organizational efficiencies. We have recently completed the syndication of the proposed new secured credit facility for the merged company. The proposed secured credit facility is expected to be comprised of a $1.85 billion term loan due 2012 and a $650 million revolving loan facility due 2011. Initial interest rate margins under the proposed secured credit facility are contemplated to be at LIBOR plus 1.75%. In addition, we have received a commitment to temporarily expand the commercial paper facility that is part of our accounts receivable securitization program by $50 million from $125 million to $175 million. Proceeds from the new credit facility, together with the expected increase in borrowings under the accounts receivable securitization program, will be used to repay outstanding borrowings under HI's existing senior secured credit facilities, Huntsman LLC's senior secured credit facilities and certain other debt. We expect to complete the merger and related financing in the third quarter of 2005. However, there can be no assurances that the new facility will be obtained. If the credit facility is not obtained, the proposed merger will not occur.

The following tables provide a summary of our structure before and after the proposed merger:

AdMat is not involved in the proposed merger and will remain our separately financed subsidiary. However, the consents we solicited in connection with the proposed merger of Huntsman LLC with and into HI would also facilitate the merger of AdMat into the merged company under certain conditions should we choose to pursue such a merger in the future.

7

Principles of Consolidation

Our condensed consolidated financial statements include the accounts of our wholly-owned and majority-owned subsidiaries and any variable interest entities for which we are the primary beneficiary.

Interim Financial Statements

Our unaudited interim condensed consolidated financial statements were prepared in accordance with accounting principles generally accepted in the United States of America ("GAAP") and in management's opinion, reflect all adjustments, consisting only of normal recurring adjustments, necessary for a fair presentation of results of operations, financial position and cash flows for the periods presented. Results for interim periods are not necessarily indicative of those to be expected for the full year. These condensed consolidated financial statements should be read in conjunction with the audited consolidated financial statements and notes to consolidated financial statements included in our Annual Report on Form 10-K for the year ended December 31, 2004.

Use of Estimates

The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates.

Reclassifications

Certain amounts in the condensed consolidated financial statements for prior periods have been reclassified to conform with the current presentation.

2. Recently Issued Accounting Pronouncements

In January 2003, the Financial Accounting Standards Board ("FASB") issued FASB Interpretation No. ("FIN") 46, "Consolidation of Variable Interest Entities." FIN 46 addresses the requirements for business enterprises to consolidate related entities, for which they do not have controlling interests through voting or other rights, if they are determined to be the primary beneficiary as a result of variable economic interests. FIN 46 provides guidance for determining the primary beneficiary for entities with multiple economic entities with multiple economic interests. Transfers to a qualifying special purpose entity are not subject to this interpretation. In December 2003, the FASB issued a replacement of FIN 46 (FIN 46R) to clarify certain complexities. We adopted this standard on January 1, 2005 and now consolidate the results of operations and financial position of Rubicon Inc. See "Note 5—Investment in Unconsolidated Affiliates".

In November 2004, the FASB issued Statement of Financial Accounting Standards ("SFAS") No. 151, "Inventory Costs—an amendment of ARB No. 43". SFAS No. 151 requires abnormal amounts of idle facility expense, freight, handling costs, and wasted material to be recognized as current-period charges. It also requires that allocation of fixed production overheads to the costs of conversion be based on the normal capacity of the production facilities. The requirements of the standard will be effective for inventory costs incurred during fiscal years beginning after June 15, 2005. We are reviewing SFAS No. 151 to determine the statement's impact on our consolidated financial statements.

In December 2004, the FASB issued SFAS No. 153, "Exchanges of Nonmonetary Assets—an amendment of APB Opinion No. 29." SFAS No. 153 addresses the measurement of exchanges of nonmonetary assets and eliminates the exception from fair value measurement for nonmonetary exchanges of similar productive assets in APB Opinion No. 29 and replaces it with an exception for exchanges that do not have commercial substance. SFAS No. 153 specifies that a nonmonetary

8

exchange has commercial substance if the future cash flows of the entity are expected to change significantly as a result of the exchange. The provisions of this standard are effective for nonmonetary exchanges occurring in fiscal periods beginning after June 15, 2005. We will apply this standard prospectively.

In December 2004, the FASB issued SFAS No. 123R, "Share Based Payment." SFAS No. 123R requires entities to measure the cost of employee services received in exchange for an award of equity instruments based on the grant-date fair value of the award. That cost will be recognized over the period during which the employee is required to provide services in exchange for the award. This standard eliminates the alternative to use the intrinsic value method of accounting for share-based payments as previously provided in APB Opinion No. 25, "Accounting for Stock Issued to Employees." We adopted SFAS No. 123R effective January 1, 2005, and have applied this standard prospectively to share-based awards issued in connection with our initial public offering. See "Note 21—Stock-Based Compensation Plans."

In March 2005, the FASB issued FIN 47, "Accounting for Conditional Asset Retirement Obligations." FIN 47 clarifies the term conditional asset retirement obligation used in SFAS No. 143, "Accounting for Asset Retirement Obligations," and clarifies when an entity would have sufficient information to reasonably estimate the fair value of an asset retirement obligation. FIN 47 is effective no later than the end of December 31, 2005. We are reviewing FIN 47 to determine its impact on our financial statements.

In March 2005, the Emerging Issues Task Force ("EITF") issued a preliminary consensus on issue 04-13, "Accounting for Purchases and Sales of Inventory with the Same Counterparty," that, if ratified by the FASB, would require companies to recognize an exchange of finished goods for raw materials or work-in-process within the same line of business at fair value. All other exchanges of inventory would be reflected at the recorded amount. We are evaluating the impact of this preliminary consensus to determine its impact on our results of operations.

In May 2005, the FASB issued SFAS No. 154, "Accounting Changes and Error Corrections—a replacement of APB Opinion No. 20 and FASB Statement No. 3." SFAS No. 154 requires retrospective application to prior periods' financial statements of changes in accounting principle, unless it is impracticable to determine either the period-specific effects or the cumulative effect of the change or unless specific transition provisions are proscribed in the accounting pronouncements. SFAS No. 154 does not change the accounting guidance for reporting a correction of an error in previously issued financial statements or a change in accounting estimate. SFAS No. 154 is effective for accounting changes and error corrections made after December 31, 2005. We will apply this standard prospectively.

3. Inventories

Inventories consisted of the following (dollars in millions):

| |

June 30, 2005 |

December 31, 2004 |

|||||

|---|---|---|---|---|---|---|---|

| Raw materials and supplies | $ | 304.8 | $ | 332.0 | |||

| Work in progress | 78.6 | 91.5 | |||||

| Finished goods | 1,019.3 | 922.8 | |||||

| Total | 1,402.7 | 1,346.3 | |||||

| LIFO reserves | (91.3 | ) | (92.0 | ) | |||

| Lower of cost or market reserves | (0.2 | ) | (0.4 | ) | |||

| Net | $ | 1,311.2 | $ | 1,253.9 | |||

9

As of June 30, 2005 and December 31, 2004, approximately 56% of inventories were recorded using the last-in, first-out cost method ("LIFO"). At June 30, 2005 and December 31, 2004, the excess of current cost over the stated LIFO value was $91.3 million and $92.0 million, respectively.

In the normal course of operations, we at times exchange raw materials and finished goods with other companies for the purpose of reducing transportation costs. No gains or losses are recorded on these exchanges, and the net open exchange positions are valued at our cost. Net amounts deducted from or added to inventory under open exchange agreements, which represent the net amounts payable or receivable by us under open exchange agreements, were approximately $0.2 million payable and $5.3 million payable (6.5 million and 8.7 million pounds) at June 30, 2005 and December 31, 2004, respectively.

4. Property, Plant and Equipment

The cost and accumulated depreciation of property, plant and equipment were as follows (dollars in millions):

| |

June 30, 2005 |

December 31, 2004 |

|||||

|---|---|---|---|---|---|---|---|

| Land | $ | 136.1 | $ | 142.1 | |||

| Buildings | 605.0 | 607.8 | |||||

| Plant and equipment | 6,161.8 | 6,367.2 | |||||

| Construction in progress | 293.8 | 251.6 | |||||

| Total | 7,196.7 | 7,368.7 | |||||

| Less accumulated depreciation | (2,388.3 | ) | (2,217.8 | ) | |||

| Net | $ | 4,808.4 | $ | 5,150.9 | |||

Depreciation expense for the three and six months ended June 30, 2005 and 2004 was $113.8 million and $138.7 million, and $230.3 million and $253.9 million, respectively.

Property, plant and equipment includes gross assets acquired under capital leases of $20.9 million and $21.5 million at June 30, 2005 and December 31, 2004, respectively; related amounts included in accumulated depreciation were $6.3 million and $6.9 million at June 30, 2005 and December 31, 2004, respectively.

10

5. Investment in Unconsolidated Affiliates

Our ownership percentage and investment in unconsolidated affiliates were as follows (dollars in millions):

| |

June 30, 2005 |

December 31, 2004 |

||||

|---|---|---|---|---|---|---|

| Equity Method: | ||||||

| Polystyrene Australia Pty Ltd. (50%) | $ | 3.4 | $ | 4.7 | ||

| Sasol-Huntsman GmbH and Co. KG (50%) | 19.9 | 17.5 | ||||

| Louisiana Pigment Company, L.P. (50%) | 120.9 | 121.6 | ||||

| Rubicon Inc. (50%)(1) | — | 5.7 | ||||

| BASF Huntsman Shanghai Isocyanate Investment BV (50%)(2) | 25.9 | 17.9 | ||||

| Others | 6.2 | 1.0 | ||||

| Total equity method investments | 176.3 | 168.4 | ||||

| Cost Method: | ||||||

| Gulf Advanced Chemicals Industry Corporation (4%) | 2.5 | 2.5 | ||||

| Total investments | $ | 178.8 | $ | 170.9 | ||

6. Intangible Assets

The gross carrying amount and accumulated amortization of intangible assets were as follows (dollars in millions):

| |

June 30, 2005 |

December 31, 2004 |

||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

Carrying Amount |

Accumulated Amortization |

Net |

Carrying Amount |

Accumulated Amortization |

Net |

||||||||||||

| Patents, trademarks, and technology | $ | 388.6 | $ | 167.7 | $ | 220.9 | $ | 411.3 | $ | 173.8 | $ | 237.5 | ||||||

| Licenses and other agreements | 14.2 | 7.5 | 6.7 | 18.3 | 10.8 | 7.5 | ||||||||||||

| Non-compete agreements and other | 57.3 | 57.3 | — | 57.7 | 57.1 | 0.6 | ||||||||||||

| Total | $ | 460.1 | $ | 232.5 | $ | 227.6 | $ | 487.3 | $ | 241.7 | $ | 245.6 | ||||||

Amortization expense was $6.5 million and $10.1 million, and $14.2 million and $20.3 million for the three and six months ended June 30, 2005 and 2004, respectively.

11

Other noncurrent assets consisted of the following (dollars in millions):

| |

June 30, 2005 |

December 31, 2004 |

||||

|---|---|---|---|---|---|---|

| Prepaid pension costs | $ | 193.0 | $ | 210.9 | ||

| Debt issuance costs, net | 58.8 | 83.9 | ||||

| Capitalized turnaround costs | 94.9 | 116.6 | ||||

| Spare parts inventory | 111.5 | 103.0 | ||||

| Catalyst assets | 11.9 | 15.2 | ||||

| Deposits | 18.2 | 16.7 | ||||

| Investment in government securities (restricted as to use) | 23.7 | — | ||||

| Other noncurrent assets | 92.5 | 62.2 | ||||

| Total | $ | 604.5 | $ | 608.5 | ||

Amortization expense of catalyst assets was $2.6 million and $2.7 million, and $4.9 million and $5.1 million for the three and six months ended June 30, 2005 and 2004, respectively.

8. Accrued Liabilities

Accrued liabilities consisted of the following (dollars in millions):

| |

June 30, 2005 |

December 31, 2004 |

||||

|---|---|---|---|---|---|---|

| Payroll and related costs | $ | 128.3 | $ | 166.5 | ||

| Interest | 116.4 | 119.3 | ||||

| Volume rebates | 69.1 | 94.4 | ||||

| Income taxes | 42.9 | 49.3 | ||||

| Taxes (property and VAT) | 61.8 | 83.0 | ||||

| Restructuring and plant closing costs | 67.7 | 122.2 | ||||

| Environmental accruals | 8.6 | 7.7 | ||||

| Pension liabilities | 24.4 | 23.1 | ||||

| Other accrued liabilities | 112.9 | 88.9 | ||||

| Total | $ | 632.1 | $ | 754.4 | ||

9. Other Noncurrent Liabilities

Other noncurrent liabilities consisted of the following (dollars in millions):

| |

June 30, 2005 |

December 31, 2004 |

||||

|---|---|---|---|---|---|---|

| Pension liabilities | $ | 503.2 | $ | 454.9 | ||

| Other postretirement benefits | 83.5 | 88.4 | ||||

| Environmental accruals | 22.2 | 27.4 | ||||

| Notes payable to affiliates | — | 29.9 | ||||

| Restructuring and plant closing costs | 30.2 | 30.9 | ||||

| Fair value of interest derivatives | 2.5 | 8.3 | ||||

| Other noncurrent liabilities | 166.2 | 117.3 | ||||

| Total | $ | 807.8 | $ | 757.1 | ||

12

10. Restructuring and Plant Closing Costs

As of June 30, 2005 and December 31, 2004, accrued restructuring and plant closing costs by type of cost and activity consisted of the following (dollars in millions):

| |

Workforce reductions(1) |

Demolition and decommissioning |

Non-cancelable lease costs |

Other restructuring costs |

Total(2) |

|||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Accrued liabilities as of December 31, 2004 | $ | 122.0 | $ | 8.4 | $ | 5.1 | $ | 17.6 | $ | 153.1 | ||||||

| 2005 charges for 2003 initiatives | 13.2 | — | — | 1.7 | 14.9 | |||||||||||

| 2005 charges for 2004 activities | 10.3 | 0.3 | 0.1 | 5.2 | 15.9 | |||||||||||

| Reversals of reserves no longer required | (0.8 | ) | — | — | (0.9 | ) | (1.7 | ) | ||||||||

| Partial reversal of AdMatTransaction opening balance sheet accrual | (3.7 | ) | (0.8 | ) | — | (0.8 | ) | (5.3 | ) | |||||||

| 2005 payments for 2003 activities | (18.2 | ) | (0.2 | ) | — | (2.4 | ) | (20.8 | ) | |||||||

| 2005 payments for 2004 activities | (44.7 | ) | (0.1 | ) | (0.5 | ) | (4.2 | ) | (49.5 | ) | ||||||

| Foreign currency effect on reserve balance | (8.3 | ) | — | — | (0.4 | ) | (8.7 | ) | ||||||||

| Accrued liabilities as of June 30, 2005 | $ | 69.8 | $ | 7.6 | $ | 4.7 | $ | 15.8 | $ | 97.9 | ||||||

| |

June 30, 2005 |

December 31, 2004 |

||||

|---|---|---|---|---|---|---|

| Accrued liabilities by activities were as follows: | ||||||

| 2001 activities | $ | 2.8 | $ | 2.8 | ||

| 2003 activities | 33.6 | 44.8 | ||||

| 2004 activities | 63.9 | 99.2 | ||||

| Foreign currency effect on reserve balance | (2.4 | ) | 6.3 | |||

| Total | $ | 97.9 | $ | 153.1 | ||

13

Details with respect to our reserves for restructuring and plant closing costs are provided below by segments and activity (dollars in millions):

| |

Polyurethanes |

Advanced Materials |

Performance Products |

Pigments |

Polymers |

Base Chemicals |

Total |

||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Accrued liabilities as of December 31, 2004 | $ | 19.0 | $ | 33.0 | $ | 58.2 | $ | 22.0 | $ | 5.8 | $ | 15.1 | $ | 153.1 | |||||||||

| 2005 charges for 2003 activities | 3.3 | — | — | 11.6 | — | — | 14.9 | ||||||||||||||||

| 2005 charges for 2004 activities | 1.1 | 0.2 | 1.4 | 5.7 | 2.9 | 4.6 | 15.9 | ||||||||||||||||

| Reversals of reserves no longer required | — | (0.8 | ) | (0.5 | ) | — | — | (0.4 | ) | (1.7 | ) | ||||||||||||

| Partial reversal of Admat Transaction opening balance sheet accrual | — | (5.3 | ) | — | — | — | — | (5.3 | ) | ||||||||||||||

| 2005 payments for 2003 activities | (3.8 | ) | (6.9 | ) | (0.8 | ) | (9.3 | ) | — | — | (20.8 | ) | |||||||||||

| 2005 payments for 2004 activities | (3.6 | ) | (5.9 | ) | (15.9 | ) | (8.9 | ) | (4.4 | ) | (10.8 | ) | (49.5 | ) | |||||||||

| Foreign currency effect on reserve balance | (1.4 | ) | (1.6 | ) | (3.2 | ) | (2.0 | ) | — | (0.5 | ) | (8.7 | ) | ||||||||||

| Accrued liabilities as of June 30, 2005 | $ | 14.6 | $ | 12.7 | $ | 39.2 | $ | 19.1 | $ | 4.3 | $ | 8.0 | $ | 97.9 | |||||||||

Current portion of restructuring reserve |

$ |

6.2 |

$ |

9.5 |

$ |

29.0 |

$ |

13.1 |

$ |

1.9 |

$ |

8.0 |

$ |

67.7 |

|||||||||

| Long-term portion of restructuring reserve | 8.4 | 3.2 | 10.2 | 6.0 | 2.4 | — | 30.2 | ||||||||||||||||

Estimated additional future charges for current restructuring projects: |

|||||||||||||||||||||||

| Estimated additional charges within one year | $ | 3.0 | $ | 0.3 | $ | 5.6 | $ | 7.8 | $ | — | $ | 1.9 | $ | 18.6 | |||||||||

Estimated additional charges beyond one year |

$ |

— |

$ |

0.1 |

$ |

— |

$ |

13.1 |

$ |

— |

$ |

4.6 |

$ |

17.8 |

|||||||||

As of June 30, 2005 and December 31, 2004, we had accruals for restructuring and plant closing costs of $97.9 million and $153.1 million, respectively. During the six months ended June 30, 2005, we recorded additional net charges of $29.2 million consisting of $29.1 million of charges payable in cash and $0.1 million of non-cash charges, for workforce reductions, demolition and decommissioning and other restructuring costs associated with closure or curtailment of activities at our smaller, less efficient manufacturing facilities. During the six months ended June 30, 2005, we made cash payments against these reserves of $70.3 million. Also during the first six months of 2005, we reversed $5.3 million of restructuring and plant closing cost accruals established in connection with the acquisition of our Advanced Materials business (the "AdMat Transaction") and recorded a corresponding credit to property, plant and equipment.

As of December 31, 2004, our Polyurethanes segment reserve consisted of $19.0 million related to various restructuring programs, including the closure of our West Deptford, New Jersey site (as announced in 2004), restructuring activities at our Rozenburg, Netherlands site (as announced in 2003), workforce reductions throughout our Polyurethanes segment (as announced in 2003), and the closure of our Shepton Mallet, U.K. site (as announced in 2002). During the six months ended June 30, 2005, our Polyurethanes segment recorded restructuring charges of $4.4 million related to these activities which was payable in cash, recorded a non-cash credit of $0.3 million to reverse prior reserves no longer required and made cash payments of $7.4 million. These restructuring activities are expected to result in additional restructuring charges of approximately $3 million. During the six months ended June 30, 2004 our Polyurethanes segment recorded restructuring charges of $22.9 million.

As of December 31, 2004, our Advanced Materials reserve accrued restructuring and plant closing costs that consisted of $33.0 million related to the restructuring programs implemented in association with the AdMat Transaction, the realignment and simplification of the commercial and technical organization and the closure of our Kaohsiung, Taiwan production facility. During the second quarter of 2005, we assessed the remaining restructuring reserves established in association with the AdMat Transaction and other 2004 initiatives and concluded that $5.3 million and $0.8 million, respectively, were no longer necessary. Accordingly, we reversed these restructuring reserves during the second quarter of 2005. The AdMat Transaction reserve reversal was recorded as a reduction to property, plant

14

and equipment in accordance with EITF 95-3, "Recognition of Liabilities in Connection with a Purchase Business Combination." The reversal of the restructuring reserve for the other 2004 initiatives was recorded as a credit to earnings. Also during the second quarter of 2005, we recorded restructuring and plant closing charges of $0.2 million for relocation and other costs. During the six months ended June 30, 2005, the Advanced Materials segment made cash payments of $12.8 million.

As of December 31, 2004, our Performance Products segment reserve consisted of $58.2 million related to various restructuring programs across our European surfactants business, including the closure of substantially all of our Whitehaven, U.K. surfactants facility, as well as the closure of our Guelph, Ontario, St. Louis, Missouri and Austin, Texas facilities. During the six months ended June 30, 2005, our Performance Products segment recorded restructuring charges of $1.8 million related to 2004 activities, $1.4 million of which is payable in cash, and a credit of $0.5 million to reverse reserves that were no longer required. The segment made cash payments of $16.7 million during the six months ended June 30, 2005. These restructuring activities are expected to result in additional restructuring charges of approximately $6 million. During the six months ended June 30, 2004, our Performance Products segment recorded restructuring charges of $20.9 million.

As of December 31, 2004, our Pigments segment reserve consisted of $22.0 million related to its global workforce reductions announced in 2003 and the reduction of its titanium dioxide ("TiO2") production capacity announced in 2004. During the six months ended June 30, 2005, our Pigments segment recorded restructuring charges of $17.3 million related to these restructuring activities, all of which is payable in cash, and made cash payments of $18.2 million. These restructuring activities are expected to result in additional restructuring charges of approximately $17 million through 2006. During July 2005, our Pigments and Base Chemicals segments announced that they would establish a single U.K. headquarters in Teesside, U.K. This will result in the closure of our Pigments segment's Billingham, U.K. headquarters and the creation of a new support center for both businesses. This restructuring activity is expected to result in additional charges of approximately $8 million, approximately $4 million of which will be incurred by the Pigments segment and approximately $4 million by the Base Chemicals segment. During the six months ended June 30, 2004, our Pigments segment recorded restructuring charges of $108.1 million.

As of December 31, 2004, our Polymers segment reserve consisted of $5.8 million related primarily to the closure of a phenol manufacturing unit in Australia and restructuring activities at our Odessa, Texas and Mansonville, Canada facilities. During the six months ended June 30, 2005, our Polymers segment recorded restructuring charges of $2.9 million related to these activities, all of which are payable in cash, and made cash payments of $4.4 million. These restructuring activities are not expected to result in any material additional restructuring charges.

As of December 31, 2004, our Base Chemicals segment reserve consisted of $15.1 million related primarily to workforce reductions arising from the announced change in work shift schedules and in the engineering and support functions at our Wilton and North Tees, U.K. facilities. During the six months ended June 30, 2005, our Base Chemicals segment recorded restructuring charges of $4.6 million, all of which was payable in cash, made cash payments of $10.8 million and recorded a credit of $0.3 to reverse reserves that were no longer required, all relating to the relocation of our corporate offices to The Woodlands, Texas and the consolidation of our U.S. purchasing functions. These restructuring activities are expected to result in additional restructuring charges of approximately $3 million through 2006. During the six months ended June 30, 2004, our Base Chemicals segment recorded restructuring charges of $2.2 million.

11. Securitization of Accounts Receivable

On December 21, 2000, we initiated an accounts receivable securitization program under which we grant an undivided interest in certain of our trade receivables to a qualified off-balance sheet entity

15

(the "Receivables Trust") at a discount. This undivided interest serves as security for the issuance of commercial paper and medium-term notes by the Receivables Trust.

At June 30, 2005 and December 31, 2004, the Receivables Trust had approximately $194.4 million and $208.4 million, respectively, in U.S. dollar equivalents in medium-term notes outstanding and approximately $18.1 million in U.S. dollar equivalents and nil, respectively, in commercial paper outstanding. The medium-term notes have a scheduled maturity date of September 15, 2006. Our commercial paper facility has a maturity date of June 30, 2007 and provides for the issuance of both euro- and U.S. dollar-denominated commercial paper up to a U.S. dollar equivalent of $125 million. We recently received a commitment to temporarily expand the commercial paper facility by $50 million to $175 million upon completion of a merger of Huntsman LLC with and into HI. The $50 million expansion would be available through March 31, 2006. Under the terms of the agreements, we and our subsidiaries continue to service the receivables in exchange for a fee of 1% of the outstanding receivables, and we are subject to recourse provisions.

Our retained interest in receivables (including servicing assets) subject to the program was approximately $336.7 million and $327.6 million as of June 30, 2005 and December 31, 2004, respectively. The value of the retained interest is subject to credit and interest rate risk. For the six months ended June 30, 2005 and 2004, new sales of accounts receivable sold into the program totaled approximately $2,890.8 million and $2,379.6 million, respectively, and cash collections from receivables sold into the program that were reinvested totaled $2,834.9 million and $2,335.1 million, respectively. Servicing fees received during the six months ended June 30, 2005 and 2004 were approximately $3.1 million and $2.6 million, respectively.

We incur losses on the accounts receivable securitization program for the discount on receivables sold into the program and fees and expenses associated with the program. We also retain responsibility for the economic gains and losses on forward contracts mandated by the terms were of the program to hedge the currency exposures on the collateral supporting the off-balance sheet debt issued. Gains and losses on forward contracts included as a component of the loss on accounts receivable securitization program were nil and a loss of $1.2 million for the six months ended June 30, 2005 and 2004, respectively. As of each of June 30, 2005 and December 31, 2004, the fair value of the open forward currency contracts was nil.

The key economic assumptions used in valuing the residual interest are presented below:

| |

June 30, 2005 |

|

|---|---|---|

| Weighted average life (in months) | Approx. 1.5 | |

| Credit losses (annual rate) | Less than 1% | |

| Discount rate (annual rate) | Approx. 1% |

A 10% and 20% adverse change in any of the key economic assumptions would not have a material impact on the fair value of the retained interest. Total receivables over 60 days past due as of June 30, 2005 and December 31, 2004 were $15.5 million and $12.1 million, respectively.

16

12. Long-Term Debt

Long-term debt outstanding as of June 30, 2005 and December 31, 2004 was as follows (dollars in millions):

| |

June 30, 2005 |

December 31, 2004 |

||||||

|---|---|---|---|---|---|---|---|---|

| Huntsman LLC Debt: | ||||||||

| Senior secured credit facilities: | ||||||||

| Revolving facility | $ | 63.0 | $ | 125.0 | ||||

| Term Loan B | 665.0 | 715.0 | ||||||

| Other debt: | ||||||||

| Huntsman LLC senior secured notes | 293.4 | 451.1 | ||||||

| Huntsman LLC senior unsecured fixed rate notes | 198.0 | 300.0 | ||||||

| Huntsman LLC senior unsecured floating rate notes | 100.0 | 100.0 | ||||||

| Huntsman LLC senior subordinated fixed rate notes | 44.2 | 44.2 | ||||||

| Huntsman LLC senior subordinated floating rate notes | 15.1 | 15.1 | ||||||

| Huntsman Specialty Chemicals Corporation subordinated note | 102.0 | 101.2 | ||||||

| Huntsman Australia Holdings Pty Ltd (HCA) credit facilities | 47.2 | 43.2 | ||||||

| HCCA credit facilities | 19.0 | 16.0 | ||||||

| Subordinated note and accrued interest—affiliate | — | 40.9 | ||||||

| Term note payable to a bank | 8.6 | 9.0 | ||||||

| Other | 3.7 | 17.5 | ||||||

| Total Huntsman LLC Debt | 1,559.2 | 1,978.2 | ||||||

HI: |

||||||||

| Senior secured credit facilities: | ||||||||

| Revolving Facility | — | — | ||||||

| Term B loan | 1,132.7 | 1,314.1 | ||||||

| Other debt: | ||||||||

| Senior unsecured notes | 455.4 | 456.0 | ||||||

| Senior subordinated notes | 1,158.1 | 1,242.0 | ||||||

| Other | 49.6 | 42.6 | ||||||

| Total HI debt | 2,795.8 | 3,054.7 | ||||||

| HIH: | ||||||||

| Senior discount notes | — | 494.7 | ||||||

| Senior subordinated discount notes—affiliate | — | 413.7 | ||||||

| Total HIH debt | — | 908.4 | ||||||

| Total HIH consolidated debt | 2,795.8 | 3,963.1 | ||||||

| AdMat: | ||||||||

| Revolving Facility | — | — | ||||||

| Senior secured notes | 348.8 | 348.6 | ||||||

| Other | 1.5 | 1.8 | ||||||

| Total AdMat debt | 350.3 | 350.4 | ||||||

| Huntsman Corporation | ||||||||

| Other | 1.3 | — | ||||||

| Total Huntsman Corporation debt | 1.3 | — | ||||||

HMP: |

||||||||

| HMP Senior Secured Notes | — | 411.9 | ||||||

| Total HMP debt | — | 411.9 | ||||||

| Fair value adjustment of HIH debt | 9.6 | |||||||

| Elimination of HIH Senior subordinated discount notes owned by HMP | — | (413.7 | ) | |||||

| Total debt | $ | 4,706.6 | $ | 6,299.5 | ||||

| Current portion | $ | 78.0 | $ | 37.5 | ||||

| Long-term portion—excluding affiliate | 4,628.6 | 6,221.1 | ||||||

| Total debt—excluding affiliate | 4,706.6 | 6,258.6 | ||||||

| Long-term debt—affiliate | — | 40.9 | ||||||

| Total debt | $ | 4,706.6 | $ | 6,299.5 | ||||

17

On May 9, 2003, HMP issued units consisting of the HMP Senior Discount Notes with an accreted value of $423.5 million and the HMP Warrants, consisting of 875,000 warrants to purchase approximately 12% of HMP's common stock. Of the $423.5 million, $8.5 million was recorded to reflect a discount of 2%, $285.0 million was recorded as the initial carrying value for the HMP Senior Discount Notes and $130.0 million was recorded as the carrying value of the warrants. The HMP Senior Discount Notes were redeemable beginning November 15, 2004 at stipulated redemption prices declining from 107.5% to 100% of accreted value by May 15, 2007. On February 28, 2005, we used proceeds from our initial public offering of common and preferred stock to redeem in full the HMP Senior Discount Notes at an accreted value of $550.0 million plus a redemption premium of $41.3 million.

Each HMP Warrant entitled the holder to purchase 0.28094 shares of HMP's common stock for an exercise price of $0.10 per share. In connection with our initial public offering, we gave notice to all holders of the outstanding HMP Warrants to exercise our rights under the terms of the HMP Warrants to require all such warrants to be exchanged for newly issued shares of our common stock. Under the terms of the HMP Warrant exchange effective on March 14, 2005, 19.57 shares of our common stock were issued in exchange for each HMP Warrant resulting in the issuance of an aggregate of approximately 16.8 million shares of our common stock in exchange for the outstanding HMP Warrants. The common stock issued in exchange for the HMP Warrants is restricted and is subject to the terms of a lock-up agreement and other applicable legal limitations on the sale of unregistered securities.

Subsidiary Debt

Our three principal operating subsidiaries are separately financed, their debt is non-recourse to us and we have no contractual obligation to fund their respective operations. Moreover, the debt of each of Huntsman LLC, HIH and AdMat is financed separately and is non-recourse to the other subsidiaries. Neither Huntsman LLC, HIH nor AdMat has any contractual obligation to fund the others' operations. The following is a discussion of the debt and liquidity of our three primary subsidiaries.

Huntsman LLC Debt

HLLC Credit Facilities

On October 14, 2004, Huntsman LLC completed a $1,065 million refinancing of its senior secured credit facilities (as refinanced, the "HLLC Credit Facilities"). On June 27, 2005, Huntsman LLC made a $50 million voluntary prepayment under the term facility portion of the HLLC Credit Facilities. Following this prepayment, the HLLC Credit Facilities consist of a $350 million revolving credit facility due October 2009 (the "HLLC Revolving Facility") and a $665 million term loan B facility due March 2010 (the "HLLC Term Facility"). Proceeds of the refinancing were used to repay in full the outstanding borrowings under Huntsman LLC's prior senior secured credit facilities. The HLLC Term Facility has scheduled annual amortization payments of $6.7 million commencing December 31, 2006, with the remaining balance due at maturity.

The HLLC Revolving Facility is secured by a first priority lien on substantially all of Huntsman LLC's current and intangible assets and those of its domestic restricted subsidiaries; and is secured by a second priority lien on substantially all of its property, plant and equipment and that of its restricted domestic subsidiaries and its indirect equity interest in HIH. The HLLC Term Facility is secured by a first priority lien on substantially all of Huntsman LLC's property, plant and equipment and that of its restricted domestic subsidiaries and its indirect equity interest in HIH; and by a second priority lien on substantially all of its current and intangible assets and those of its restricted domestic subsidiaries. The

18

HLLC Credit Facilities are also guaranteed by Huntsman Specialty Chemicals Holdings Corporation and Huntsman Specialty and by Huntsman LLC's domestic restricted subsidiaries (collectively, the "HLLC Guarantors"). Neither HIH nor HI is a restricted subsidiary of Huntsman LLC and they are not HLLC Guarantors.

The HLLC Revolving Facility is subject to a borrowing base of accounts receivable and inventory and is available for general corporate purposes. Borrowings under the HLLC Revolving Facility bear interest, at Huntsman LLC's option, at a rate equal to (i) a LIBOR-based eurocurrency rate plus an applicable margin of 2.25%, or (ii) a prime-based rate plus an applicable margin of 1.25%. The HLLC Revolving Facility allows Huntsman LLC to borrow up to $50 million secured by letters of credit; however, the $350 million revolving credit facility is reduced dollar-for-dollar by any letters of credit outstanding.

As of June 30, 2005, the weighted average interest rate on Huntsman LLC's senior credit facilities was 6.3%, excluding the impact of interest rate hedges. As of June 30, 2005, the HLLC Revolving Facility and HLLC Term Facility bear interest at LIBOR plus 2.25% per year and LIBOR plus 3.0% per year, respectively. In accordance with the HLLC Term Facility agreement, as a result of our initial public offering of common and preferred stock and the use of offering proceeds for the permanent reduction of indebtedness by Huntsman LLC, the HLLC Term Facility interest rate margin decreased from LIBOR plus 3.50% to LIBOR plus 3.0%.

The agreements governing the HLLC Credit Facilities contain customary financial covenants; covenants relating to the incurrence of debt, the purchase and sale of assets, limitations on investments and affiliate transactions; change of control provisions; events of default provisions; and acceleration provisions. Management believes that Huntsman LLC is in compliance with the covenants of the HLLC Credit Facilities.

HLLC Senior Secured Notes

On September 30, 2003, Huntsman LLC sold $380 million aggregate principal amount of 11.625% senior secured notes due October 15, 2010 at an issue price of 98.8% (the "September 2003 Offering"). On December 3, 2003, Huntsman LLC sold an additional $75.4 million aggregate principal amount of senior secured notes (collectively with the notes sold in the September 2003 Offering, the "HLLC Senior Secured Notes") at an issue price of 99.5%. Interest on the HLLC Senior Secured Notes is payable semiannually on April 15 and October 15. The effective interest rate is 11.9%. The HLLC Senior Secured Notes are effectively subordinated to all of Huntsman LLC's obligations under the HLLC Revolving Facility and rank pari passu with the HLLC Term Facility. The HLLC Senior Secured Notes are guaranteed by the HLLC Guarantors.

The HLLC Senior Secured Notes are redeemable after October 15, 2007 at 105.813% of the principal amount thereof, declining ratably to par on and after October 15, 2009. At any time prior to October 15, 2006, Huntsman LLC may redeem up to 35% of the original aggregate principal amount of the HLLC Senior Secured Notes at a redemption price of 111.625% with the net cash proceeds of a qualified equity offering. As a result of our initial public offering of common and preferred stock, Huntsman LLC redeemed 35%, or approximately $159.4 million, of the aggregate principal amount of the HLLC Senior Secured Notes on February 28, 2005 and paid a call premium of approximately $18.5 million. Following this partial redemption of the HLLC Senior Secured Notes, there remain approximately $296.0 million in aggregate principal amount of the HLLC Senior Secured Notes outstanding.

The indenture governing the HLLC Senior Secured Notes contains covenants relating to the incurrence of debt, limitations on distributions, asset sales and affiliate transactions, among other things. The indenture also requires Huntsman LLC to offer to repurchase the HLLC Senior Secured

19

Notes upon a change of control. Management believes that Huntsman LLC is in compliance with the covenants of the HLLC Senior Secured Notes.

HLLC Senior Notes

On June 22, 2004, Huntsman LLC sold $300 million of its senior unsecured fixed rate notes that bear interest at 11.5% and mature on July 15, 2012 (the "HLLC Unsecured Fixed Rate Notes") and $100 million of its senior unsecured floating rate notes that bear interest at a rate equal to LIBOR plus 7.25% and mature on July 15, 2011 (the "HLLC Unsecured Floating Rate Notes," and together with the HLLC Unsecured Fixed Rate Notes, the "HLLC Senior Notes"). The interest rate on the HLLC Unsecured Floating Rate Notes as of June 30, 2005 was approximately 10.4%. Interest on the HLLC Unsecured Fixed Rate Notes is paid each January 15 and July 15 and is paid on the HLLC Unsecured Floating Rate Notes on the 15th of January, April, July and October. The proceeds from the offering of the HLLC Senior Notes were used to repay $362.9 million on Huntsman LLC's prior term loan B facility and $25 million to repay indebtedness at HCCA. See "—Other Debt" below. The HLLC Senior Notes are unsecured obligations of Huntsman LLC and are guaranteed by the HLLC Guarantors.

The HLLC Unsecured Fixed Rate Notes are redeemable after July 15, 2008 at 105.75% of the principal amount thereof, declining ratably to par on and after July 15, 2010. The HLLC Unsecured Floating Rate Notes are redeemable after July 15, 2006 at 104.0% of the principal amount thereof, declining ratably to par on and after July 15, 2008. At any time prior to July 15, 2007, Huntsman LLC may redeem up to 40% of the original aggregate principal amount of the HLLC Unsecured Fixed Rate Notes at a redemption price of 111.5% with proceeds of a qualified equity offering. At any time prior to July 15, 2006, Huntsman LLC may redeem up to 40% of the aggregate original principal amount of the HLLC Unsecured Floating Rate Notes with the proceeds of a qualified equity offering at a redemption price equal to the par value plus LIBOR plus 7.25%. As a result of our initial public offering of common and preferred stock, Huntsman LLC redeemed 34%, or approximately $102.0 million of combined aggregate principal amount of the HLLC Unsecured Fixed Rate Notes on March 14 and March 17, 2005 with combined call premiums of approximately $11.7 million. Following this partial redemption, there remain approximately $198.0 million in aggregate principal amount of the HLLC Unsecured Fixed Rate Notes outstanding.

The indenture governing the HLLC Senior Notes contains covenants relating to the incurrence of debt and limitations on distributions, asset sales and affiliate transactions, among other things. The indenture also requires Huntsman LLC to offer to repurchase the HLLC Senior Notes upon a change of control. Management believes that Huntsman LLC is in compliance with the covenants.

HLLC Notes

Huntsman LLC's 9.5% fixed and variable subordinated notes due 2007 (the "HLLC Notes") with an outstanding principal balance of $59.3 million as of June 30, 2005 are unsecured subordinated obligations of Huntsman LLC and are junior in right of payment to all of its existing and future secured or unsecured senior indebtedness and effectively junior to any of its secured indebtedness to the extent that collateral secures such indebtedness. Interest is payable on the HLLC Notes semiannually on January 1 and July 1 at an annual rate of 9.5% on the fixed rate notes and LIBOR plus 3.25% on the floating rate notes. The HLLC Notes are redeemable at Huntsman LLC's option after July 2002 at a price declining from 104.75% to 100% of par value as of July 1, 2005. The weighted average interest rate on the floating rate notes was approximately 6.0% as of June 30, 2005. As a result of previously executed amendments to the indentures, virtually all the restrictive covenants contained in the indentures have been eliminated.

On August 2, 2005, Huntsman LLC issued a notice of redemption for all of the outstanding HLLC Notes in accordance with the amended and restated indenture governing the HLLC Notes. Accordingly,

20

at the time of the Proposal Merger of Huntsman LLC with and into HI, we will deliver sufficient funds to the trustee to redeem the HLLC Notes, in full, on September 1, 2005.

Other Debt

Huntsman Specialty's subordinated note, in the aggregate principal amount of $75.0 million, accrued interest until April 15, 2002 at 7% per annum. Pursuant to the note agreement, effective April 15, 2002, all accrued interest was added to the principal of the note for a total principal amount of $106.6 million. Such principal balance will be payable in a single installment on April 15, 2008. Interest has been payable quarterly in cash, commencing July 15, 2002. For financial reporting purposes, the note was initially recorded at its estimated fair value of $58.2 million, based on prevailing market rates as of the effective date. As of June 30, 2005 and December 31, 2004, the unamortized discount on the note was $4.6 million and $5.4 million, respectively. We have given notice that we intend to redeem these notes, in full, at the time of the proposed merger of Huntsman LLC with and into HI.

Huntsman Corporation Australia Pty Ltd. ("HCA"), Huntsman LLC's indirect Australian subsidiary that holds its Australian surfactants assets, maintains credit facilities (the "HCA Facilities"). As of June 30, 2005, borrowings under the HCA Facilities totaled A$62.4 million ($47.2 million), which include A$41.0 million ($31.1 million) on the term loan facility and A$21.4 million ($16.1 million) on the revolving credit line. On August 31, 2004, HCA refinanced the previously existing debt facilities with an A$30.0 million ($23.1 million) revolving credit line supported by a borrowing base of eligible accounts receivable and inventory and an A$44.0 million ($33.9 million) term facility.

Huntsman Chemical Company Australia Pty Ltd. ("HCCA") and certain Australian affiliates hold Huntsman LLC's Australian styrenics assets. On August 31, 2004, HCCA refinanced the previously existing debt facilities of HCCA with an A$30.0 million ($23.1 million) revolving credit line supported by a borrowing base of eligible accounts receivable (the "HCCA Facility"). As of June 30, 2005, borrowings under the HCCA Facility totaled A$24.9 million ($19.0 million).

The HCA Facilities and the HCCA Facility are secured by a lien on substantially all their respective assets, bear interest at a rate of 2.9% above the Australian base rate, mature in August 2007 and are non-recourse to Huntsman LLC. As of June 30, 2005, the interest rate on the HCA Facilities and the HCCA Facility was approximately 8.6%. On June 24, 2004, Huntsman LLC used $25 million of proceeds from the offering of the HLLC Senior Unsecured Notes to repay a portion of the previously existing debt facilities of HCCA. Management believes that HCA and HCCA are in compliance with the covenants of the HCA Facilities and the HCCA Facility.

On July 2, 2001, Huntsman LLC entered into a 15% note payable (the "Affiliate Note") with an affiliated entity in the amount of $25.0 million. Interest on the Affiliate Note was not paid in cash, but accrued at a designated effective rate of 15% per annum, compounded annually. On February 16, 2005, the Affiliate Note was satisfied in full from proceeds of Huntsman Corporation's initial public offering. As of December 31, 2004 and February 16, 2005, accrued interest added to the principal balance was $15.9 million and $16.6 million, respectively.

HI Debt

HI Credit Facilities

As of June 30, 2005, HI had senior secured credit facilities (the "HI Credit Facilities") which consisted of a revolving loan facility of up to $375 million maturing in September 2008 (the "HI Revolving Facility"), which includes a $50 million multicurrency revolving loan facility available in euros, GBP Sterling and U.S. dollars, and a term loan B facility consisting of a $1,082.5 million term portion and a €41.6 million (approximately $50.2 million) term portion (the "HI Term Facility"). On

21

March 24, 2005, and June 6, 2005, HI made voluntary payments of $75.0 million and $100 million dollar equivalents, respectively, on the HI Term Facility. The maturity of the HI Term Facility is December 31, 2010; provided that the maturity will be accelerated to December 31, 2008 if HI has not refinanced all of the outstanding HI Senior Notes and the HI Subordinated Notes (as defined below) on or before December 31, 2008 on terms satisfactory to the administrative agent under the HI Credit Facilities. Scheduled amortization of the HI Term Facility is approximately $11.4 million per annum commencing June 30, 2006, with the remaining unpaid balance due at maturity. The HI Credit Facilities allow HI to borrow up to $100 million secured by letters of credit; however, the $375 million revolving credit facility is reduced dollar-for-dollar by any letters of credit outstanding. As of June 30, 2005, there were no loans outstanding on the HI Revolving Facility, and there were $6.9 million in letters of credit outstanding.

Interest rates for the amended and restated HI Credit Facilities are based upon, at HI's option, either a eurocurrency rate (LIBOR) or a base rate (prime) plus the applicable spread. The applicable spreads vary based on a pricing grid, depending on the loan facility and whether specified conditions have been satisfied, in the case of eurocurrency-based term loans, from 2.25% to 2.50% per annum for term loan B dollar loans and from 3.00% to 3.25% per annum for term loan B euro loans, and, in the case of base rate term loans, from 1.00% to 1.25% per annum for term B dollar loans. The applicable spread for eurocurrency-based revolving loans ranges from 2.25% to 3.25% and for base rate revolving loans from 1.00% to 2.00%. As of June 30, 2005, the weighted average interest rate on the HI Credit Facilities was approximately 5.5%, excluding the impact of interest rate hedges.

The HI Credit Facilities are secured by a first priority lien on substantially all HI's assets and all the assets of its domestic subsidiaries and certain of its foreign subsidiaries. The HI Credit Facilities are also guaranteed by HIH, HI's domestic subsidiaries and certain of its foreign subsidiaries (the "HI Guarantors").

The agreements governing the HI Credit Facilities contain customary financial covenants; covenants relating to the incurrence of debt, the purchase and sale of assets, limitations on investments and affiliate transactions; change in control provisions; events of default provisions; and acceleration provisions. Management believes that HI is in compliance with the covenants of the HI Credit Facilities.

HI Senior Notes and HI Subordinated Notes

In March 2002, HI sold $300 million aggregate principal amount of HI Senior Notes that are due in 2009. On April 11, 2003, HI sold an additional $150 million aggregate principal amount of the HI Senior Notes at an issue price of 105.25%. Net proceeds from the sale of these notes were used to repay amounts outstanding under the HI Credit Facilities. The HI Senior Notes are unsecured obligations. Interest on the HI Senior Notes is payable semiannually in March and September. The HI Senior Notes are redeemable after March 1, 2006 at 104.937% of the principal amount thereof, declining ratably to par on and after March 1, 2008.

On December 17, 2004, HI completed an offering of $175 million of its 7.375% senior subordinated notes due 2015 and €135 million of its 7.5% senior subordinated notes due 2015 (the "HI Senior Subordinated Notes due 2015"). HI used all of the net proceeds to redeem part of its outstanding 10.125% senior subordinated notes due 2009 (the "HI Senior Subordinated Notes due 2009" and, together with the HI Senior Subordinated Notes due 2015, the "HI Senior Subordinated Notes"). Prior to the partial redemptions discussed below, HI had outstanding $600 million and € 450 million of the HI Senior Subordinated Notes due 2009. The HI Senior Subordinated Notes due 2009 became redeemable on July 1, 2004 at 105.063% of the principal amount thereof, which declines ratably to par on and after July 1, 2007. HI redeemed $231 million and €77 million of Senior Subordinated Notes due 2009 on December 31, 2004 and $2.9 million and €1.0 million of Senior

22

Subordinated Notes due 2009 on January 3, 2005. In connection with these redemptions, HI paid approximately $17.0 million and $0.2 million in U.S. dollar equivalents in redemption premiums on December 31, 2004 and January 3, 2005, respectively.

As of December 31, 2004, following the December 31, 2004 partial redemption of the HI Senior Subordinated Notes due 2009, HI had outstanding $369 million and €373 million of Senior Subordinated Notes due 2009 and $175 million and €135 million of HI Senior Subordinated Notes due 2015, for a combined total of $544 million and €508 million of HI Senior Subordinated Notes plus $5.3 million of unamortized premium. As of June 30, 2005, HI had outstanding $366.1 million and €372.0 million of HI Senior Subordinated Notes due 2009 and $175 million and €135 million of HI Senior Subordinated Notes due 2015, for a combined total of $541.1 million and €507.0 million of HI Senior Subordinated Notes plus $4.3 million of unamortized premium. The $175 million and €135 million HI Senior Subordinated Notes due 2015 are redeemable on or after January 1, 2010 at 103.688% and 103.750%, respectively, of the principal amount thereof, which declines ratably to par on and after January 1, 2013. In addition, at any time prior to January 1, 2008, HI may redeem up to 40% of the original aggregate principal amount of the $175 million and €135 million Senior Subordinated Notes due 2015 at redemption prices of 107.375% and 107.5% plus accrued and unpaid interest, respectively. The HI Senior Subordinated Notes are unsecured and interest is payable semiannually in January and July of each year.

The HI Senior Notes and the HI Senior Subordinated Notes contain covenants relating to the incurrence of debt, limitations on distributions, asset sales and affiliate transactions, among other things. They also contain a change of control provision requiring HI to offer to repurchase the HI Senior Notes and the HI Subordinated Notes upon a change of control. Management believes that HI is in compliance with the covenants of the HI Senior Notes and the HI Senior Subordinated Notes.

On December 10, 2004, HI entered into a cross-currency interest rate swap. The cross-currency swap requires HI to pay euros and receive U.S. dollars at the maturity date of January 1, 2010. The U.S. dollar notional amount is $175 million and bears interest at a fixed rate of 7.375%, payable semiannually on January 1 and July 1. The euro notional amount is approximately €132 million and bears interest at a blended fixed rate of approximately 6.63%, payable semiannually on January 1 and July 1.

Other Debt

HI maintains a $25 million multicurrency overdraft facility used for the working capital needs for its European subsidiaries (the "HI European Overdraft Facility"). As of June 30, 2005 and December 31, 2004, there were no borrowings outstanding under the HI European Overdraft Facility.